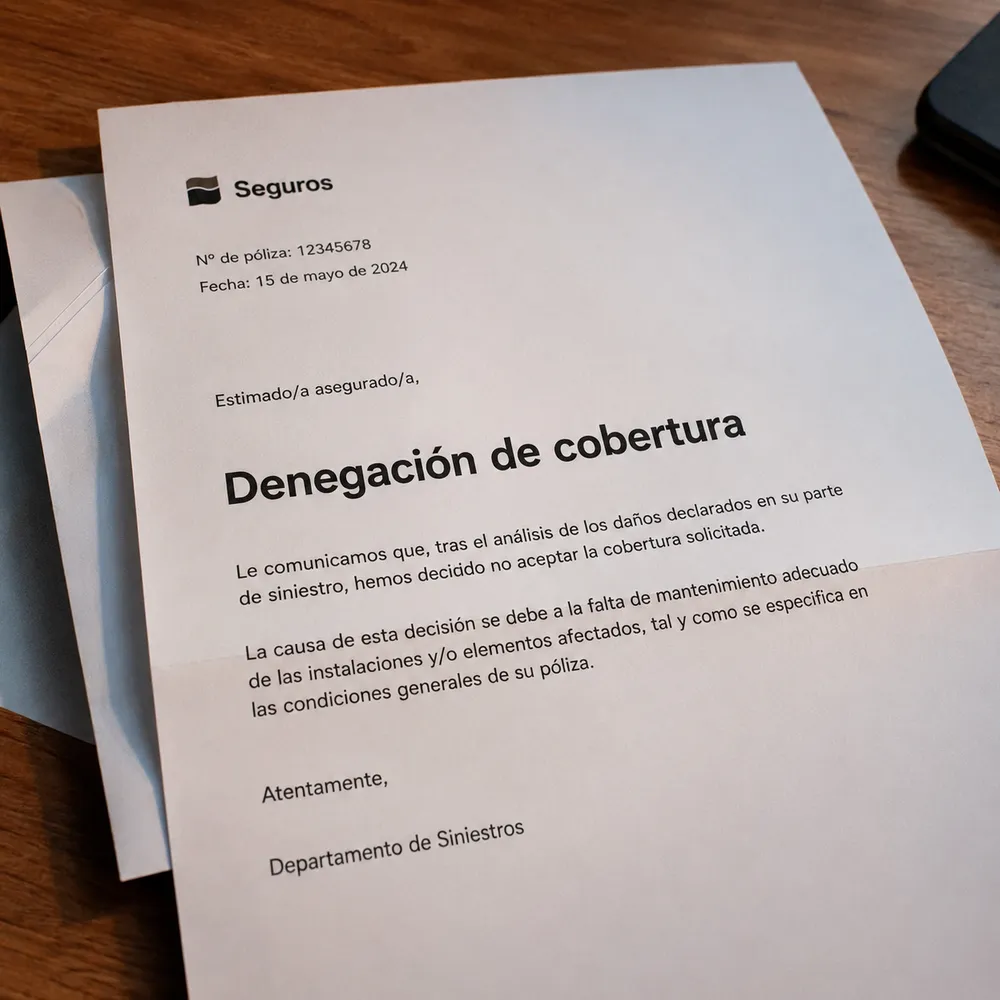

Insurance Denied: The Lack of Maintenance Trap

Imagine the scene: a pipe bursts at home, water ruins your living room floor, and after the initial shock, you breathe a sigh of relief thinking, "Thank goodness I have insurance." You notify the company, the loss adjuster visits, and a few days later, you receive the dreaded notice: claim rejected due to lack of maintenance.

In the insurance sector, claim denials under this argument are one of the main sources of conflict, frustration, and complaints. What the policyholder sees as a sudden, unforeseen accident, the company views as the inevitable consequence of long-term neglect. But where is the line between an accident and a lack of upkeep?

The Root of the Problem: What Does Insurance Actually Cover? To understand the conflict, we must look at the foundation of an insurance contract. By law, policies are designed to cover risks that are uncertain, future, and unforeseen. A pipe bursting due to excess pressure is a clear accident. However, a slow leak through a worn-out shower silicone seal over several years is not; it is considered a predictable physical process resulting from the passage of time.

Home, business, and community policies explicitly exclude damage caused by natural wear and tear, rust, or lack of conservation. The contract requires the owner to act with due diligence, keeping the property in optimal condition to prevent risks from materializing. The problem arises when companies use this clause as a "catch-all" to avoid paying for claims that should actually be covered.

The Most Common Rejection Scenarios Alleged lack of maintenance rarely gives a warning; it is discovered when the adjuster examines the root of the problem. The most common cases typically focus on three critical areas:

Plumbing and bathrooms: Damp patches appearing on hallway walls because the shower tray silicone is cracked or the tile grout has worn away, slowly leaking water every time someone showers.

Roofs and terraces: Leaks after heavy rainfall where the insurer claims that the drains were blocked by leaves and dirt, or that the waterproofing membrane had exceeded its lifespan without being replaced.

Electrical installations: Short circuits in obsolete systems that lack proper thermal protection or suffer from overloads due to age.

The Economic Impact of Rejection When a company denies a claim based on this argument, the financial impact on the insured party is usually twofold. On one hand, repairing the source of the problem is always the owner's responsibility (insurance will never pay to re-seal a shower or replace an old pipe).

On the other hand, and more importantly, by estimating that the cause is a lack of maintenance, the company usually rejects the consequential damages as well. This means the neighbor's damaged ceiling or your own ruined flooring are not covered either, leaving you completely stranded with very high bills.

A key legal point in your favor: The burden of proof rests on the insurer. The company cannot reject a claim based on mere guesswork; it must prove through a rigorous and objective technical report that the damage is exclusively and directly due to neglect and not an accidental event. An older property has every right to be insured and have its claims covered, provided there is no blatant abandonment.

What Should You Do If Your Claim Is Rejected? If you receive a denial that you disagree with, it is essential to follow these steps:

Request the adjuster's report in writing: It is your legal right. Demand the full document showing the exact technical justification for the rejection.

Arrange an independent assessment: If you are convinced the damage was accidental, hire an independent loss adjuster or surveyor to evaluate the area and issue a counter-report.

Formal complaint: File a formal complaint with your insurer's Customer Service Department, attaching your favorable report. If this fails, you can escalate the case to the official Insurance Ombudsman or regulatory body.